Liability insurance is a crucial form of coverage that provides financial protection for individuals and businesses in the event of legal claims or lawsuits. But what exactly is liability insurance, and how does it work? Let’s break it down:

- Definition: Liability insurance is a type of insurance policy that protects the insured party against claims made by third parties for property damage, bodily injury, or other losses caused by the insured’s actions or negligence.

- Coverage: Liability insurance typically covers legal expenses, including attorney fees, court costs, and settlements or judgments, arising from covered claims. This coverage extends to a variety of scenarios, such as accidents on your property, injuries caused by your products or services, or defamation claims.

- Types of Liability Insurance:

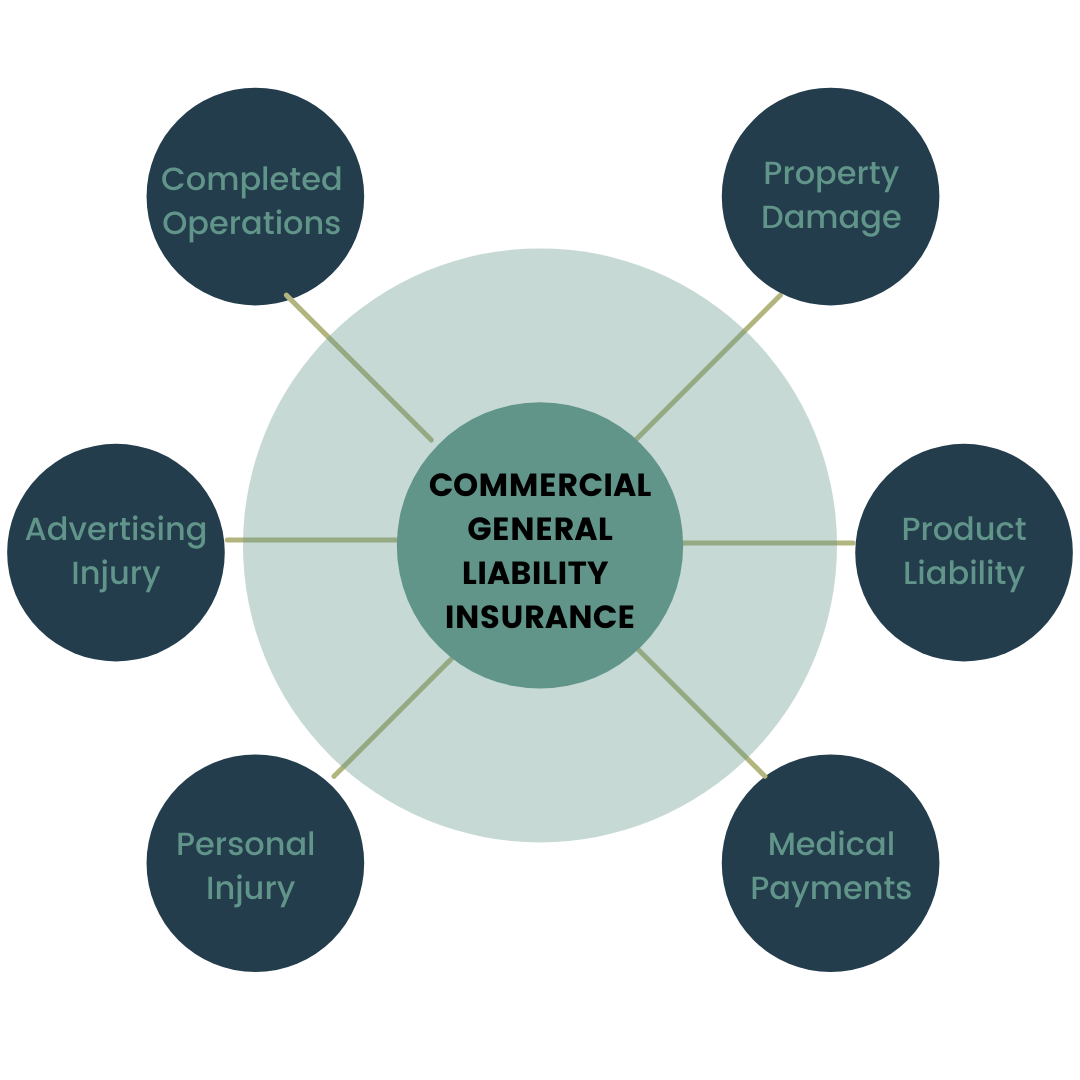

- General Liability Insurance: Provides coverage for common risks faced by businesses, such as slip-and-fall accidents, property damage, and advertising injuries.

- Professional Liability Insurance: Also known as errors and omissions insurance, it protects professionals (e.g., doctors, lawyers, consultants) against claims of negligence or failure to perform professional duties.

- Product Liability Insurance: Covers manufacturers, distributors, and retailers against claims related to defective products that cause harm or injury to consumers.

- Public Liability Insurance: Similar to general liability insurance, it covers claims arising from accidents or injuries that occur in public spaces owned or operated by the insured.

- Employer’s Liability Insurance: Provides coverage for claims made by employees for work-related injuries or illnesses not covered by workers’ compensation insurance.

- Importance: Liability insurance is essential for protecting individuals and businesses from financial losses associated with legal claims or lawsuits. Without liability insurance, you could be personally responsible for paying damages awarded in a lawsuit, potentially leading to financial ruin.

- Legal Requirements: In some cases, liability insurance may be required by law or contractually obligated by clients or business partners. For example, many states mandate businesses to carry certain types of liability insurance, such as workers’ compensation insurance or general liability insurance.

- Cost: The cost of liability insurance varies depending on factors such as the type of coverage, the industry, the size of the business, and the level of risk. However, compared to the potential financial losses associated with a lawsuit, the cost of liability insurance is relatively affordable.

In summary, liability insurance is a crucial component of risk management for individuals and businesses, providing financial protection against legal claims and lawsuits. By understanding what liability insurance is and how it works, you can make informed decisions to protect yourself, your assets, and your business from unforeseen liabilities.